South Africa’s agricultural sector has more than doubled in value and volume terms since 1994. This success has been linked to international trade. Exports now account for roughly half (in value terms) of the annual agricultural production.

Other drivers have been improvements in productivity through crop and animal genetics.

Exports are largely to the rest of the African continent. In 2023, these accounted for 38% of South Africa’s agricultural exports. The EU is another important market for South Africa’s agricultural sector, accounting for a 19% share in 2023.

In recent years, Asia and the Far East, in particular China, have been identified by the agriculture sector and policymakers as the key growth frontiers.

Asia and the Middle East accounted for a quarter of South Africa’s agricultural exports in 2023. But huge pockets of opportunity remain, in terms of products and countries.

China is the biggest opportunity, largely because of its population and economic size. China, the world’s second-largest economy after the US, must feed 1.4 billion people. To do this, China is a huge importer, resulting in an agricultural trade deficit with the rest of the world of about US$117 billion. This suggests there’s a gap for countries with good agricultural offerings.

South Africa has lagged behind its competitors in gaining from this growth in Chinese imports. It stands at number 32 in the list of countries that supply China with food. South Africa’s agricultural exports to China accounted for a mere 0.4% of Chinese imports in 2023.

Read: South Africa targets China as key market for its farm produce

China’s size warrants more attention than it typically receives from South African policymakers. The South African agricultural sector – I am the chief economist of the Agricultural Business Chamber of South Africa – has been calling for greater efforts to increase South African exports to China.

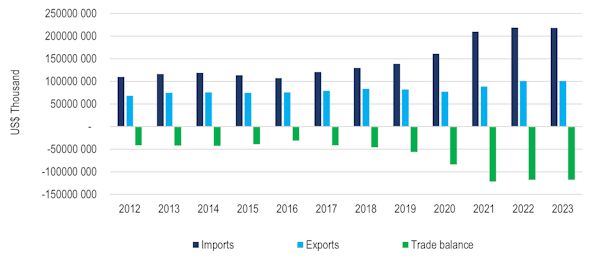

China’s agricultural trade

Source: Trade Map and Agbiz Research

China’s top agricultural imports include oilseeds, meat, grains, fruits and nuts, cotton, beverages and spirits, sugar, wool, and vegetables.

South Africa is already an exporter of these products to various countries in the world and is producing surpluses for some. This means there is room to expand to China, especially as South Africa’s agricultural production continues to increase and with more volume expected in the coming years.

It, therefore, makes sense for South Africa to focus more on widening export markets to China.

This means arguing for a broad reduction in import tariffs that China currently levies on some of the agricultural products from South Africa.

Removing phytosanitary constraints in various products is also key.

There is room for more ambitious export efforts. Three government departments must lead the conversation – Trade, Industry and Competition; Agriculture; and International Relations and Cooperation.

What’s holding South Africa back

South Africa has strong political ties with China, bilaterally and through the umbrella group known as Brics and the Forum for China-Africa Cooperation. But these forums are primarily political, not trade blocs.

What South Africa doesn’t have is preferential market access to China’s food markets.

This hobbles South African farmers who compete for the Chinese market with Australian and Chilean producers. Australia and Chile have secured trade agreements that give them competitive advantage.

The lack of an agreement that secures better access for South African producers means they face substantial trade barriers. The main ones are:

- China’s high import tariffs;

- Phytosanitary constraints on various products, including rules about production methods (like the use of antibiotics); and

- Slower trade facilitation methods, like China’s requirement that citrus products wait for 24 days before being allowed entry, which adds costs.

What China buys

China’s key agricultural imports include soybeans, cotton, malt, beef, palm oil, wool, wine, fruits, nuts, pork and barley. South Africa is among the top 10 global agricultural exporters of most fruits and a significant producer of wine.

South Africa’s current major exports to China are wool, citrus, nuts, sugar, wine, maize, soybeans, beef and grapes. With the exception of wool, South Africa’s market share of these products remains negligible.

Listen/read: What does the Agriculture and Agro-Processing Master Plan hope to achieve?

South Africa expects an increase in the production of various fruits and nuts in the coming years from trees that have already been planted.

The wine industry also continues to see decent volumes of production. The same is true for the red meat industry, which is on a path to grow and to expand its export markets.

The producers of all these products could benefit from wider access to China.

What’s to be done

South Africa stands as an anomaly among the top global agricultural exporters with limited market access to China for various products.

If China is to be an area of focus for export-led growth in agriculture, a new way of engaging will be essential to soften the current trade barriers.

Firstly, a strategic approach to the Chinese agricultural markets needs to be adopted. This would entail dedicated teams from both South African and Chinese departments of agriculture that would deal with details of trade barriers.

Listen:

Do we need stronger trade agreements with China?

‘Regardless of leadership, we should continue on the path set for agriculture’

Secondly, South Africa should use the Brics platform – of which China is also a member – to call for deepening of agricultural trade among the Brics members. This would help add momentum to the bilateral engagements of South Africa and China.

Thirdly, South Africa should encourage foreign direct investment – in particular Chinese investors – in agriculture for new production in areas which have large tracts of underutilised land. These include the Eastern Cape, KwaZulu-Natal and Limpopo provinces.

Having Chinese nationals as partners in agricultural development could help boost trade and business ties between the two countries.

Lastly, China provides a good base for the demand for higher-value agricultural products, which South Africa intends to focus on in its development agenda.![]()

Wandile Sihlobo, Senior Fellow, Department of Agricultural Economics, Stellenbosch University

This article is republished from The Conversation under a Creative Commons licence. Read the original article.

Follow Moneyweb’s in-depth finance and business news on WhatsApp here.

COMMENTS 1

You must be signed in to comment.

SIGN IN SUBSCRIBE

or create a free account.

Free users can leave 4 comments per month.

Subscribers can leave unlimited comments via our website and app.

What competitive advantages does the local farmer have over his international competition?

American companies, Cargill, Monsanto, and Dupont, own more than 50% of farmland in Ukraine. Ukraine produces 22 million tonnes on 4 million hectares. The average local farmer owns less than a thousand hectares and the industry produces 1.8 million tonnes.

Their cost of fuel and fertilizer is much lower than in South Africa while their cost of capital is a fraction of local interest rates. Their average wheat yield is 5 tonnes per hectare while locals struggle to average 3.4 tonnes per hectare.

The previous low interest rate cycle motivated major international pension funds to invest in farmland, rather than government bonds that offered zero yield. These pension funds have a constant flow of new cash every month that is looking for opportunities. Their cost of capital is very low compared to local farmers who borrow at 10% interest or more.

These major grain companies and pension funds cause overproduction that floods the market and puts downward pressure on the price, pushing the yields of international farmers down to that of EU government bonds.

Why will China pay higher prices for South African produce if they can import from Ukraine, Russia, and Australia at more competitive prices? Like Sasol, PetroSA, and Denel, the last time local grain producers had a competitive advantage was during the protective period of sanctions under the previous government.

End of comments.